“Fall Seven Times, Stand up Eight”-Naoki Higashida

Ever wanted to own a piece of your favorite Japanese gaming company? Look no further!

The onset of Covid-19 pandemic has been nothing but trouble for the economy and almost all industries. However, there are some industries for whom the pandemic has proved to be a turning point, and among those are video games and online gaming.

The wonderful quote above by Naoki Higashida captures the essence of all that is gaming. Games capture the minds & imaginations of kids and adults alike and all it takes is a single controller to convert a stern, disciplined adult into a laughing, smiling kid.

The global video game industry is now poised to grow in leaps and bounds. E-sports which are gaming competitions have seen a rise in viewership and revenue. A new generation of sportspeople are emerging; one which bucks tradition.

Covid-19 has shown a new future of sports: a future in which all the activity takes place on a monitor and the rules of the game have changed. Japan, which is synonymous with the Golden Age of gaming, and where video gaming is a major industry, is expected to be a major beneficiary of this growth.

In this article, we will look at 8 such gaming companies expected to benefit from this gaming boom.

The World:

The world gaming market was valued at 151 billion USD at end of 2019 with it being forecasted to grow at 9.2% Compound Annual Growth Rate (CAGR).

Asia pacific region holds the majority of the revenue share at 47% and is set to continue to dominate the global gaming market.

The Asia pacific region is currently valued at 77.9 billion USD and is poised to grow at 8.2% CAGR.

China is expected to have a major share of this market due to their large population & Japan holds the second largest share of the market.

World E-sports Market

What began as an amateur get together to show off gaming skills and win bragging rights sometime in late 2000s has been transformed into a multibillion dollar industry. The world E-sports market is currently valued at 1.1 billion USD and looks likely to grow at a healthy 16.1% CAGR.

North America holds the larger share beating Asia pacific by a narrow margin.

Within the Asia pacific region, Japan holds the second largest E-Sports market share at 61.2 million USD.

Asia Pacific E-sports market revenue is projected to grow at a respectable 13.2% CAGR.

Japan

With its world famous exports from the 80’s and 90’s, Japan is rightly associated with video gaming. Video games are a major industry in Japan, with the three gaming giants, Sony, Nintendo and Sega having formed during the golden age alongside several other familiar names like Namco, Capcom, Square Enix, Konami.

The golden age of gaming is also associated with the rise of video game arcades in which Japan was a dominant player. Even today, despite the world having moved on to personal gaming devices and consoles, arcades continue to enjoy immense popularity with Japanese gamers.

Japan’s gaming market was valued at 18.9 billion USD and is expected to grow at 4.2% CAGR.

Japan has a strong E-sports environment and its E-sports revenue is expected to grow at 12.2% CAGR.

Consoles & Mobile gaming

The future of gaming is said to be on mobile and a lot of focus is on mobile games at the moment. However, consoles are the preferred choice of gaming for households in Japan.

Japan continues to maintain a strong presence in the console hardware market with two of the three dominant world players in Japan (Sony and Nintendo).

Microsoft has found it difficult to enter the Japanese console market with the vast majority of Japanese consumers preferring their domestic counterparts.

Japan is also making great strides in mobile gaming with around 70 million active players.

This continuous rise in mobile gaming has been given a massive boost by the Covid-19 lockdown and the mobile gaming industry today stands at an inflection point. Japan’s mobile gaming companies are expected to benefit from this as they receive worldwide adoption.

The Japanese government is also supportive of the Japanese gaming industry and it has now extend its support to the E-sports industry as well. It is planning to expand Japan’s E-Sports industry with the private sector to help revitalize regional economies and generate 285 billion JPY a year by 2025.

Japan’s video game industry stands at an interesting time in its illustrious history. It has a lot of tailwinds (Covid-19 induced demand, government support, increased reach and adoptions amongst customers worldwide) and very few headwinds. It already leads the console and mobile gaming segment and has the potential to increase its market share while expanding to other geographies as well.

Let’s look at 8 of these gaming companies in Japan.

1. Nintendo

Founded in 1889 as a manufacturer of playing cards, Nintendo has grown & matured across its more than a century’s journey into a giant conglomerate consisting of 25 subsidiaries engaged in development, manufacture and sale of consoles, videogames, playing cards and other entertainment products.

Its largest game brand and one which it is well known for is its Pokémon, which also had a hugely popular card game in the laste 1990’s and early 2000’s. It has also published a series of home and handheld consoles but is a smaller player in comparison to SONY & Microsoft.

Series of Home Consoles:

Series of Handheld consoles

Some of the game series published by Nintendo are as follows:

Nintendo produces off the wall consoles which appeal to customers of all age groups, especially children.

With its name already familair in the west from it’s smash hits Super Nintendo and Nintendo 64, the company firmly planted itself as the console of choice for families in 2006, with its array of fun-looking games which could be played by al family members.

During the PS4 vs Xbox One years, it came out with the Switch and was a surprise hit as it gained mass popularity due to its dual nature of home console & handheld console.

Nintendo has also made clear their intention of extending and supporting the life of the Switch and are reportedly planning some new launched at present.

Nintendo’s share price has increased dramatically in 2020, with a leap of 6% in August on news of its success due to the hugely popular Animal Crossing during the lockdown period. Many analysts believe the share price still has plenty of room to grow.

Financials: (Source: https://in.tradingview.com/symbols/TSE-7974/) (All figures except share price in USD) (USD Rate 1 USD = 104.76)

| Valuation | Price History | ||

| Market Capitalization | 63.9B | Average Volume (10 day) | 658.64K |

| Enterprise Value (MRQ) | 42.7B | 1-Year Beta | 0.5583 |

| Enterprise Value/EBITDA (TTM) | 10.34 | 52 Week High | 61.3K |

| Total Shares Outstanding (MRQ) | 119.124M | 52 Week Low | 31.88K |

| Number of Employees | 6.2K | ||

| Number of Shareholders | 37.775K | Dividends | |

| Price to Earnings Ratio (TTM) | 19.2262 | Dividends Paid (FY) | -1.0B |

| Price to Revenue Ratio (TTM) | 4.4835 | Dividends Yield (FY) | 1.7956 |

| Price to Book (FY) | 4.3492 | Dividends per Share (FY) | 10.4 |

| Price to Sales (FY) | 5.1208 | ||

| Margins | |||

| Balance Sheet | Net Margin (TTM) | 0.2332 | |

| Quick Ratio (MRQ) | 3.7954 | Gross Margin (TTM) | 0.5151 |

| Current Ratio (MRQ) | 4.0449 | Operating Margin (TTM) | 0.3143 |

| Debt to Equity Ratio (MRQ) | 0.0119 | Pretax Margin (TTM) | 0.3274 |

| Net Debt (MRQ) | -11.82B | ||

| Total Debt (MRQ) | 0.17B | Income Statement | |

| Total Assets (MRQ) | 18.85B | Basic EPS (FY) | 20.73 |

| Basic EPS (TTM) | 27.93 | ||

| Operating Metrics | EPS Diluted (FY) | 20.73 | |

| Return on Assets (TTM) | 0.1951 | Net Income (FY) | 2.5B |

| Return on Equity (TTM) | 0.2405 | EBITDA (TTM) | 4.6B |

| Return on Invested Capital (TTM) | 0.2376 | Gross Profit (MRQ) | 2.0B |

| Revenue per Employee (TTM) | 2.01M | Gross Profit (FY) | 6.1B |

| Last Year Revenue (FY) | 12.5B | ||

| Total Revenue (FY) | 12.5B |

Nintendo has seen steady revenue growth since the launch of the Switch and Covid-19 seems to have not affected it much. The company is also projected to grow its revenue and at this stage their prospects look strong.

Nintendo has regained its high profit margin which is amongst the highest in the industry. Its margins reflect the superior loyalty and following which Nintendo enjoys which we predict it will continue to enjoy.

2. Sony

Sony Corporation (known as SONY) founded in 1946 develops, designs, manufactures & sells electronic equipment, instruments, devices, game consoles & games and software for consumers, professionals and industrial markets. Its subsidiary, Sony Interactive Entertainment LLC handles the console and game publishing business. SONY is famous for one of the world’s bestselling and most popular console series the PlayStation.

It also develops & publishes console exclusive games through its subsidiary companies. It is believed that the high quality and increasing no. of exclusive games offered by SONY has led to the huge popularity and sale of the PlayStation series. Some of its games are as follows:

SONY’s rivalry with fellow console maker and largest competitor Microsoft is well known and the two are now clashing again with the release of their respective latest generation of console: the PlayStation 5 and Xbox Series X.

Unlike other stocks mentioned in this article, Sony Corp. is an enormous company and its video game business accounts for 27.3% of its revenue, meaning that when you buy Sony stock, less than a third is going towards owning its video game business — so it’s important to check out the other part of the business, too!

Financials: (Source: https://in.tradingview.com/symbols/TSE-6758/) (All figures except share price in USD) (USD Rate 1 USD = 104.76)

| Valuation | Price History | ||

| Market Capitalization | 92.3B | Average Volume (10 day) | 4.38M |

| Enterprise Value (MRQ) | 79.9B | 1-Year Beta | 0.9192 |

| Enterprise Value/EBITDA (TTM) | 4.3038 | 52 Week High | 8.92K |

| Total Shares Outstanding (MRQ) | 1.221B | 52 Week Low | 5.297K |

| Number of Employees | 111.7K | ||

| Number of Shareholders | 423.556K | Dividends | |

| Price to Earnings Ratio (TTM) | 14.9395 | Dividends Paid (FY) | -0.4B |

| Price to Revenue Ratio (TTM) | 1.1865 | Dividends Yield (FY) | 0.6332 |

| Price to Book (FY) | 2.3354 | Dividends per Share (FY) | 0.43 |

| Price to Sales (FY) | 1.2098 | ||

| Margins | |||

| Balance Sheet | Net Margin (TTM) | 0.0799 | |

| Quick Ratio (MRQ) | 0.8407 | Gross Margin (TTM) | 0.3353 |

| Current Ratio (MRQ) | 0.9337 | Operating Margin (TTM) | 0.1018 |

| Debt to Equity Ratio (MRQ) | 0.4703 | Pretax Margin (TTM) | 0.107 |

| Net Debt (MRQ) | -1517.594B | ||

| Total Debt (MRQ) | 19.4B | Income Statement | |

| Total Assets (MRQ) | 225.5B | Basic EPS (FY) | 4.5 |

| Basic EPS (TTM) | 5.2 | ||

| Operating Metrics | EPS Diluted (FY) | 4.4 | |

| Return on Assets (TTM) | 0.0293 | Net Income (FY) | 5.5B |

| Return on Equity (TTM) | 0.1622 | EBITDA (TTM) | 15.2B |

| Return on Invested Capital (TTM) | 0.1337 | Gross Profit (MRQ) | 6.1B |

| Revenue per Employee (TTM) | 0.7M | Gross Profit (FY) | 27B |

| Last Year Revenue (FY) | 78.63B | ||

| Total Revenue (FY) | 78.63B | ||

| Free Cash Flow (TTM) | 10.4B |

Sony has seen steady revenue growth across past few years with there being a dip in 2020. It has projected sales to remain subdued for FY 2021 due to Covid-19 but expects revenue to pick up with the launch of PlayStation 5 and several games with it. Their PlayStation Plus subscription service has also seen a boost of 2.7 million users bringing the user base to 41.5 million.

Source: https://finance.yahoo.com/quote/SNE/financials/, https://www.marketscreener.com/quote/stock/SONY-CORPORATION-6492482/financials/

Sony’s Net Profit margin have seen consistent growth but had to take a hit due to Covid-19. The same can be expected to return to normal once economy resumes

Home video game equipment, world share 57%. In the fiscal year ended March 31, 2018, operating income increased by approximately 200 billion yen due to the impact of the earthquake and loss of impairment. The quantity of PS4 has been further increased by expanding the software.

3. Konami

Konami founded in 1969 is a Japanese entertainment and gambling conglomerate. It develops, manufactures and distributes trading cards, anime, slot machines & arcade machines. It also develops and publishes video games. It has casinos around the world and runs health & physical fitness clubs around Japan.

Some of the famous game series developed by Konami are as follows:

Financials: Source: https://in.tradingview.com/symbols/TSE-9766/ (All figures except share price in USD) (USD Rate 1 USD = 104.76)

| Valuation | Price History | ||

| Market Capitalization | 5.4B | Average Volume (10 day) | 467.4K |

| Enterprise Value (MRQ) | 3.8B | 1-Year Beta | 1.3528 |

| Enterprise Value/EBITDA (TTM) | 5.7356 | 52 Week High | 5.19K |

| Total Shares Outstanding (MRQ) | 133.214M | 52 Week Low | 2.461K |

| Number of Employees | 5.057K | ||

| Number of Shareholders | 21.673K | Dividends | |

| Price to Earnings Ratio (TTM) | 34.043 | Dividends Paid (FY) | -133.5M |

| Price to Revenue Ratio (TTM) | 2.1903 | Dividends Yield (FY) | 1.074 |

| Price to Book (FY) | 2.0816 | Dividends per Share (FY) | 0.5 |

| Price to Sales (FY) | 2.19 | ||

| Margins | |||

| Balance Sheet | Net Margin (TTM) | 0.0648 | |

| Quick Ratio (MRQ) | 1.8664 | Gross Margin (TTM) | 0.3851 |

| Current Ratio (MRQ) | 1.9653 | Operating Margin (TTM) | 0.1809 |

| Debt to Equity Ratio (MRQ) | 0.1483 | Pretax Margin (TTM) | 0.104 |

| Net Debt (MRQ) | -883.3M | ||

| Total Debt (MRQ) | 384.2M | Income Statement | |

| Total Assets (MRQ) | 4.03B | Basic EPS (FY) | 1.41 |

| Basic EPS (TTM) | 1.19 | ||

| Operating Metrics | EPS Diluted (FY) | 1.38 | |

| Return on Assets (TTM) | 0.0407 | Net Income (FY) | 189.8M |

| Return on Equity (TTM) | 0.0623 | EBITDA (TTM) | 697.4M |

| Return on Invested Capital (TTM) | 0.0601 | Gross Profit (MRQ) | 217.9M |

| Revenue per Employee (TTM) | 0.5M | Gross Profit (FY) | 947.6M |

| Last Year Revenue (FY) | 2.5B | ||

| Total Revenue (FY) | 2.5B |

The company has mentioned of several projects in the works but the fallout with Metal Gear Solid creator Hideo Kojima means that a lot of them might be in trouble. The company has assured that they are moving on with the new projects even those initially developed by Kojima. However, fan reactions to them will be known with time.

They have also switched their focus from single player games to multi-player games and have now begun to focus on mobile gaming. Konami’s European president Masami Saso has declared in no uncertain terms that E-sports will form major part of Konami’s future games development.

The company established Esports Ginza Studio in Tokyo, which is equipped with state of the art equipment for e-sports in November 2019 with a view to hosting major competitions.

They have had growing revenues coinciding with their new mobile game launches, and they have reduced their revenue projections suggesting that they are spending a lot of money on research & development and not on launch of new products, but they expect this research to turn into profit in 2022.

Their Net Profit Margin has therefore reduced recently, but the new product launches might help get them back on track.

Source: https://www.investing.com/equities/konami-corp.-balance-sheet

4. Nexon

Nexon Co. is a South Korean- Japanese video game publisher that specializes in online games for PC and Mobile. It has been credited for introducing the world’s first graphic Massively Multiplayer Online Role Playing Game (MMORPG) and the first free-to-play game of its kind. It is the industry pioneer of MMORPGs with more than 80 live games operated across more than 190 countries. Some of its games are as follows:

Financials: Source: https://in.tradingview.com/symbols/TSE-3659/ (All figures except share price in USD) (USD Rate 1 USD = 104.76)

| Valuation | Price History | ||

| Market Capitalization | 21.2B | Average Volume (10 day) | 4.358M |

| Enterprise Value (MRQ) | 16.4B | 1-Year Beta | 0.455 |

| Enterprise Value/EBITDA (TTM) | 7.3675 | 52 Week High | 2.965K |

| Total Shares Outstanding (MRQ) | 885.898M | 52 Week Low | 1.225K |

| Number of Employees | 6.428K | ||

| Number of Shareholders | 2.881K | Dividends | |

| Price to Earnings Ratio (TTM) | 19.6234 | Dividends Paid (FY) | 0 |

| Price to Revenue Ratio (TTM) | 8.8318 | Dividends Yield (FY) | 0.2028 |

| Price to Book (FY) | 3.5084 | Dividends per Share (FY) | 0.02 |

| Price to Sales (FY) | 8.937 | ||

| Margins | |||

| Balance Sheet | Net Margin (TTM) | 0.4533 | |

| Quick Ratio (MRQ) | 11.3845 | Gross Margin (TTM) | 0.7647 |

| Current Ratio (MRQ) | 11.3845 | Operating Margin (TTM) | 0.4254 |

| Debt to Equity Ratio (MRQ) | 0.0184 | Pretax Margin (TTM) | 0.5013 |

| Net Debt (MRQ) | -4.4B | ||

| Total Debt (MRQ) | 116M | Income Statement | |

| Total Assets (MRQ) | 7.3B | Basic EPS (FY) | 1.23 |

| Basic EPS (TTM) | 1.21 | ||

| Operating Metrics | EPS Diluted (FY) | 1.22 | |

| Return on Assets (TTM) | 0.1556 | Net Income (FY) | 1.1B |

| Return on Equity (TTM) | 0.1792 | EBITDA (TTM) | 1.08B |

| Return on Invested Capital (TTM) | 0.1773 | Gross Profit (MRQ) | 476.2M |

| Revenue per Employee (TTM) | 0.4M | Gross Profit (FY) | 1.8B |

| Last Year Revenue (FY) | 2.7B | ||

| Total Revenue (FY) | 2.7B |

Nexon’s five major franchises on PC have generated billions of revenue over the years. It now plans to bring them all to mobile which will increase its revenue multifold. They have benefited a lot from the pandemic lockdown.

Their franchises are gaining popularity and receiving love from new and veteran gamers alike. They have also decided to expand towards other countries, mostly in North America.

Nexon has seen steady revenue growth and projected to continue growing at a similar rate

Source: https://www.investing.com/equities/nexon-co-ltd-balance-sheet

https://www.marketscreener.com/quote/stock/NEXON-CO-LTD-10016656/?type_recherche=rapide&mots=nexon

They have phenomenally high net profit margins and with the popularity they enjoy, will continue to maintain it.

5. Square Enix

Square Enix founded in 1975 is a Japanese video game company that develops and sells video games for home consoles as well as online. The company also publishes guidebooks for its games and comic magazines and books.

Some of its famous game series are as follows:

Financials: Source: https://in.tradingview.com/symbols/TSE-9684/ (All figures except share price in USD) (USD Rate 1 USD = 104.76)

| Valuation | Price History | ||

| Market Capitalization | 7.3B | Average Volume (10 day) | 785.81K |

| Enterprise Value (MRQ) | 5.1B | 1-Year Beta | 0.459 |

| Enterprise Value/EBITDA (TTM) | 11.3691 | 52 Week High | 7.46K |

| Total Shares Outstanding (MRQ) | 119.316M | 52 Week Low | 3.695K |

| Number of Employees | 5.077K | ||

| Number of Shareholders | 15.357K | Dividends | |

| Price to Earnings Ratio (TTM) | 24.3547 | Dividends Paid (FY) | -5.3M |

| Price to Revenue Ratio (TTM) | 2.5875 | Dividends Yield (FY) | 0.8385 |

| Price to Book (FY) | 3.4639 | Dividends per Share (FY) | 0.5 |

| Price to Sales (FY) | 2.8994 | ||

| Margins | |||

| Balance Sheet | Net Margin (TTM) | 0.1062 | |

| Quick Ratio (MRQ) | 3.1045 | Gross Margin (TTM) | 0.497 |

| Current Ratio (MRQ) | 4.5258 | Operating Margin (TTM) | 0.1685 |

| Debt to Equity Ratio (MRQ) | 0.0196 | Pretax Margin (TTM) | 0.1554 |

| Net Debt (MRQ) | -1.08B | ||

| Total Debt (MRQ) | 4.3M | Income Statement | |

| Total Assets (MRQ) | 2.8B | Basic EPS (FY) | 1.709 |

| Basic EPS (TTM) | 2.529 | ||

| Operating Metrics | EPS Diluted (FY) | 1.706 | |

| Return on Assets (TTM) | 0.1104 | Net Income (FY) | 203.7M |

| Return on Equity (TTM) | 0.1446 | EBITDA (TTM) | 549.9M |

| Return on Invested Capital (TTM) | 0.1418 | Gross Profit (MRQ) | 484.9M |

| Revenue per Employee (TTM) | 0.5M | Gross Profit (FY) | 1.2B |

| Last Year Revenue (FY) | 2.5B | ||

| Total Revenue (FY) | 2.5B |

They have declared launch of new games which include one on Marvel’s Avengers which has been released recently and has received average reviews but has been a well-selling game.

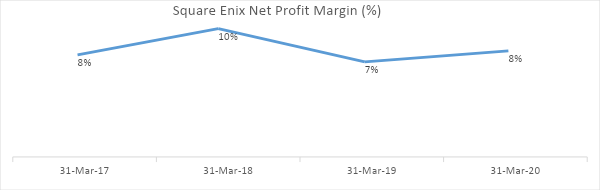

They have seen steady revenues and are projecting higher revenue for coming years due to the new game launches

Source: https://www.investing.com/equities/square-enix-holdings-co-ltd-income-statement

https://www.marketscreener.com/quote/stock/SQUARE-ENIX-HOLDINGS-CO–6494078/financials/

Their net profit margin has been lackluster and has fluctuated but the same is again showing signs of improvement.

Probably best known for its Final Fantasy series, the company made the news in August 2020 when more than 5 million Final Fantasy VII Remake copies were sold at launch. But there is more to come! That was only the first part; the second part will follow a year or two later and it seems predictable that those who played the first part will be the first to buy it when it’s out.

This also begs the question of whether they will resurrect another of the other Final Fantasy classics (anyone else an FF9 fan?).

6. CyberAgent

Cyber Agent is a Japanese digital advertisement and game publishing company founded in 1998. They started Cygames in 2009 and it along with 12 other gaming subsidiaries develop and operate mobile games. Some of its titles are as follows:

Financials: Source: https://in.tradingview.com/symbols/TSE-4751/ (All figures except share price in USD) (USD Rate 1 USD = 104.76)

| Valuation | Price History | ||

| Market Capitalization | 8.1B | Average Volume (10 day) | 718.07K |

| Enterprise Value (MRQ) | 6.4B | 1-Year Beta | 0.4651 |

| Enterprise Value/EBITDA (TTM) | 13.1246 | 52 Week High | 7.03K |

| Total Shares Outstanding (MRQ) | 126.093M | 52 Week Low | 3.175K |

| Number of Employees | 5.139K | ||

| Number of Shareholders | 15.404K | Dividends | |

| Price to Earnings Ratio (TTM) | 155.7658 | Dividends Paid (FY) | -3.8M |

| Price to Revenue Ratio (TTM) | 1.9045 | Dividends Yield (FY) | 0.4911 |

| Price to Book (FY) | 10.5709 | Dividends per Share (FY) | 0.3 |

| Price to Sales (FY) | 1.9681 | ||

| Margins | |||

| Balance Sheet | Net Margin (TTM) | 0.0123 | |

| Quick Ratio (MRQ) | 2.5047 | Gross Margin (TTM) | 0.2939 |

| Current Ratio (MRQ) | 2.5283 | Operating Margin (TTM) | 0.0766 |

| Debt to Equity Ratio (MRQ) | 0.485 | Pretax Margin (TTM) | 0.0555 |

| Net Debt (MRQ) | -639M | ||

| Total Debt (MRQ) | 393.8M | Income Statement | |

| Total Assets (MRQ) | 2.2B | Basic EPS (FY) | 0.128 |

| Basic EPS (TTM) | 0.439 | ||

| Operating Metrics | EPS Diluted (FY) | 0.117 | |

| Return on Assets (TTM) | 0.0257 | Net Income (FY) | 16.1M |

| Return on Equity (TTM) | 0.0705 | EBITDA (TTM) | 422.7M |

| Return on Invested Capital (TTM) | 0.0472 | Gross Profit (MRQ) | 305.4M |

| Revenue per Employee (TTM) | 0.8M | Gross Profit (FY) | 1.2B |

| Last Year Revenue (FY) | 4.3B | ||

| Total Revenue (FY) | 4.3B |

Cygames has an E-sports team which participates in street fighter competition. They have also launched a subsidiary Cymusic which will produce music. In addition they have some games lined up for release.

Cyber Agent has seen steady revenue rise and have projected for a similar growth in revenues.

Source: https://www.investing.com/equities/cyberagent-inc-balance-sheet

Nintendo has acquired 5% stake in Cygames as they collaborated on & released a new game called Dragalia Lost Read. This marked Nintendo’s foray in mobile gaming segment and further development in that area will lead to better opportunities for Cygames and Cyber Agent in the future.

Subsidiary CyberZ started collaboration with Avex Entertainment Inc. and esports event “RAGE” in March 2017, and has grown into one of the largest esports competitions in Japan, mobilizing 10,000 people in a year and a half.

7. Bandai Namco

Bandai Namco, founded in 2006 by a Merger of gaming giants Bandai & Namco, is a Japanese Multinational video game developer and publisher. It has developed and published several successful game franchise, a few of which are mentioned below:

In addition they have also published several mobile and online games. They have also decided to focus on new products going forward.

Financials: Source: https://in.tradingview.com/symbols/TSE-7832/ (All figures except share price in USD) (USD Rate 1 USD = 104.76)

| Valuation | Price History | ||

| Market Capitalization | 16.3B | Average Volume (10 day) | 509.94K |

| Enterprise Value (MRQ) | 10.6B | 1-Year Beta | 0.9351 |

| Enterprise Value/EBITDA (TTM) | 9.4798 | 52 Week High | 8.004K |

| Total Shares Outstanding (MRQ) | 219.629M | 52 Week Low | 4.57K |

| Number of Employees | 9.052K | ||

| Number of Shareholders | 30.129K | Dividends | |

| Price to Earnings Ratio (TTM) | 31.6504 | Dividends Paid (FY) | -308.5M |

| Price to Revenue Ratio (TTM) | 2.4034 | Dividends Yield (FY) | 0.5408 |

| Price to Book (FY) | 3.7971 | Dividends per Share (FY) | 1.3 |

| Price to Sales (FY) | 2.3574 | ||

| Margins | |||

| Balance Sheet | Net Margin (TTM) | 0.076 | |

| Quick Ratio (MRQ) | 1.7287 | Gross Margin (TTM) | 0.3606 |

| Current Ratio (MRQ) | 2.2354 | Operating Margin (TTM) | 0.1069 |

| Debt to Equity Ratio (MRQ) | 0.1107 | Pretax Margin (TTM) | 0.1037 |

| Net Debt (MRQ) | -1.2B | ||

| Total Debt (MRQ) | 465.5M | Income Statement | |

| Total Assets (MRQ) | 6.1B | Basic EPS (FY) | 2.50 |

| Basic EPS (TTM)245.3684 | 2.34 | ||

| Operating Metrics | EPS Diluted (FY) | 2.50 | |

| Return on Assets (TTM) | 0.0894 | Net Income (FY) | 550.4M |

| Return on Equity (TTM) | 0.1259 | EBITDA (TTM) | 958.5M |

| Return on Invested Capital (TTM) | 0.1223 | Gross Profit (MRQ) | 555.3M |

| Revenue per Employee (TTM) | 0.76M | Gross Profit (FY) | 2.5B |

| Last Year Revenue (FY) | 6.9B | ||

| Total Revenue (FY) | 6.9B |

Bandai Namco had pretty stable revenue so far but has projected almost double its usual revenue to be bolstered by sales from its its Dragon Ball franchise.

Source: https://www.investing.com/equities/bandai-namco-holdings-inc-balance-sheet

It has pretty stable net profit margin and the same is expected to continue in the foreseeable future

The company’s popular game “Tekken 7” was adopted at the world’s largest fighting game event “EVO” in 2018 and has been a feature each year since.

8. Capcom

Capcom, established in 1979, began as a manufacturer of arcade game machines and transitioned into a video game developer and publisher.

It has developed legendary game series like Resident Evil, Devil May Cry, Mega Man, Street Fighter etc. Street Fighter has now gained prominence amongst E-sports enthusiasts and is one of the major games in E-Sports.

Financials: Source: https://in.tradingview.com/symbols/TSE-9697/ (All figures except share price in USD) (USD Rate 1 USD = 104.76)

| Valuation | Price History | ||

| Market Capitalization | 6.1B | Average Volume (10 day) | 566.09K |

| Enterprise Value (MRQ) | 3.4B | 1-Year Beta | 0.7006 |

| Enterprise Value/EBITDA (TTM) | 11.87 | 52 Week High | 6.34K |

| Total Shares Outstanding (MRQ) | 106.75M | 52 Week Low | 2.4K |

| Number of Employees | 2.988K | ||

| Number of Shareholders | 10.273K | Dividends | |

| Price to Earnings Ratio (TTM) | 34.7998 | Dividends Paid (FY) | -4M |

| Price to Revenue Ratio (TTM) | 7.306 | Dividends Yield (FY) | 0.7525 |

| Price to Book (FY) | 6.4006 | Dividends per Share (FY) | 0.4 |

| Price to Sales (FY) | 7.824 | ||

| Margins | |||

| Balance Sheet | Net Margin (TTM) | 0.2099 | |

| Quick Ratio (MRQ) | 3.2169 | Gross Margin (TTM) | 0.794 |

| Current Ratio (MRQ) | 4.2312 | Operating Margin (TTM) | 0.2957 |

| Debt to Equity Ratio (MRQ) | 0.0628 | Pretax Margin (TTM) | 0.2954 |

| Net Debt (MRQ) | -602.1M | ||

| Total Debt (MRQ) | 6.2M | Income Statement | |

| Total Assets (MRQ) | 1.3B | Basic EPS (FY) | 1.43 |

| Basic EPS (TTM) | 1.64 | ||

| Operating Metrics | EPS Diluted (FY) | 1.43 | |

| Return on Assets (TTM) | 0.1436 | Net Income (FY) | 152.2M |

| Return on Equity (TTM) | 0.1869 | EBITDA (TTM) | 273.9M |

| Return on Invested Capital (TTM) | 0.1785 | Gross Profit (MRQ) | 198.9M |

| Revenue per Employee (TTM) | 0.26M | Gross Profit (FY) | 625.5M |

| Last Year Revenue (FY) | 778.8M | ||

| Total Revenue (FY) | 778.8M |

Capcom is soon to launch three major titles which will be providing a boost to their revenue. The company has also launched its games on mobile and the response has been positive domestically. It is also looking to transition to a multi-platform game developer as it launched the game “Shinsekai: Into the Depth” for Apple Arcade.

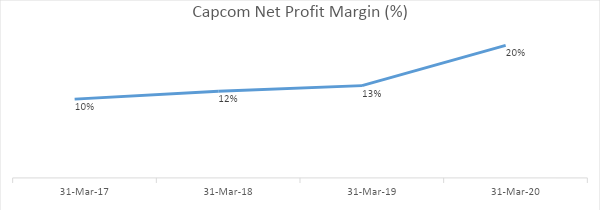

Revenue has been more or less steady and their projections are in line with the past trend.

Source: https://www.investing.com/equities/capcom-co-ltd

https://www.marketscreener.com/quote/stock/CAPCOM-CO-LTD-6492670/financials/

Net Profit margin for Capcom however has seen improvement doubling from 4 years ago.

Capcom has declared plans to bring dormant IPs back to life which include Dino Crisis and Darkstalkers which might bring back old fans and customers.

The company set up a game experience space “CAPCOM eSPORTS Club” in Kichijoji, Tokyo which holds events regularly.

Conclusion:

The future for gaming worldwide looks bright. Japan, which is quick to take to new technology will once again be the first ones to participate in the gaming revolution. The future for Japanese video game industry looks brighter still, and it might be a good idea to “press start” on some of these awesome gaming stocks and enter the game before it’s too late!