“We never learn what hidden gems lie along the paths we do not explore”

Unknown

In investing, just like in life, there are hidden gems on the paths we do not explore.

The Nikkei 225 consisting of the largest and most popular companies of Japan is at a 5 year high.

There are several hidden gems among Japanese companies which are still undervalued because they are not commonly known inside Japan, let alone outside of Japan!

In this article we present five of the best undervalued equities in the Japanese stock market.

Each of these companies stands out by being highly profitable with business models which are hard to imitate. Let’s have a look at their financials.

| Company name | Market Cap (JPY) | Gross Profit Margin (%) | Operating Profit Margin (%) | Net Profit Margin (%) | Current Ratio |

| Benefit One Inc. (Ticker: 2412) | 487.75 Billion | 39.7% | 21.9% | 15.1% | 1.91 |

| Keyence (Ticker: 6861) | 12.63 Trillion | 81.8% | 50.3% | 35.9% | 15.24 |

| OBIC (Ticker: 4684) | 1.89 Trillion | 70.0% | 55.7% | 43.6% | 7.65 |

| M3 Inc. (Ticker: 2413) | 6.09 Trillion | 55.7% | 26.2% | 18.4% | 3.19 |

| Asahi Intecc Co Ltd (Ticker: 7747) | 932.97 Billion | 67.3% | 22.6% | 16.2% | 3.74 |

Benefit One

Benefit One is a Japan based company engaged in corporate welfare schemes as well as other membership services. Its focus is on providing fringe benefit services like car plans and health insurance to the employees of its client companies.

It has global operations with offices in countries such as United States, Germany, China, Thailand, Indonesia and Singapore with nearly eight million members in Japan alone.

It has even acquired Rewardz, a Singapore based HR solution provider that integrates traditional corporate benefit programs into an app that allows users to track and visualize their progress.

The business has a consistently growing revenue profile with decent profit margins with operating profits at 21.9% and Net Profit Margins at 15.1%.

It has virtually zero debt and a healthy current ratio. It has also maintained and even improved its margin considerably and consistently. The company is 10% away from all-time highs and is looking set to make a new high.

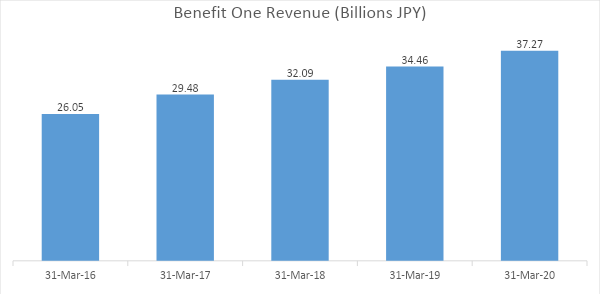

| All figures in Billions JPY except EPS and Ratios | 31-Mar-20 | 31-Mar-19 | 31-Mar-18 | 31-Mar-17 | 31-Mar-16 |

| Revenue | 37.27 | 34.46 | 32.09 | 29.48 | 26.05 |

| Gross Profit | 14.80 | 13.77 | 12.58 | 12.03 | 10.24 |

| Depreciation | 0.16 | 0.18 | 0.33 | 0.20 | 0.21 |

| Interest | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Operating Income | 8.16 | 7.54 | 6.16 | 5.85 | 4.34 |

| PAT | 5.63 | 5.15 | 4.16 | 3.81 | 2.68 |

| EPS | 36.29 | 32.68 | 26.49 | 24.43 | 34.76 |

| Operating Margin | 21.9% | 21.9% | 19.2% | 19.9% | 16.7% |

| Net Profit Margin | 15.1% | 14.9% | 13.0% | 12.9% | 10.3% |

| Gross Margin | 39.7% | 40.0% | 39.2% | 40.8% | 39.3% |

| Current Assets | 23.47 | 28.04 | 23.48 | 20.27 | 16.18 |

| Cash | 8.46 | 12.82 | 10.42 | 7.40 | 4.79 |

| Current Liabilities | 12.30 | 13.88 | 12.21 | 11.14 | 9.43 |

| LT Debt | 0.18 | 0.22 | 0.23 | 0.29 | 0.13 |

| Equity | 16.57 | 19.87 | 17.07 | 14.68 | 11.85 |

| ST Debt | 0.16 | 0.17 | 0.13 | 0.27 | 0.00 |

| Maturity of LT | 0.12 | 0.11 | 0.11 | 0.12 | 0.07 |

| Current Ratio | 1.91 | 2.02 | 1.92 | 1.82 | 1.72 |

| Debt to Equity | 0.03 | 0.03 | 0.03 | 0.05 | 0.02 |

| Cash to Equity | 0.02 | 0.03 | 0.02 | 0.02 | 0.01 |

With companies looking to increase their engagement with their employees working at home and with a need to provide additional rewards that will serve as morale boosters, Benefit One looks to be benefiting the most with an even higher margin and strong revenue growth.

Benefit One also features in our article on 9 Japanese Stocks with High ROE.

Keyence Corporation

Despite being fairly unknown in the west, Keyence Corporation is a global behemoth which is now the third largest company in Japan by market capitalization. The company has a reputation for paying some of the highest salaries in Japan.

Keyence develops and manufactures factory automation systems which include automation sensors, vision systems, barcode readers, laser markers, measuring instruments and digital microscopes amongst others.

It undertakes its manufacturing via contract manufacturing, preferring to stick to their core competence of design and development.

It has a strong global network of 220 offices in 46 countries serving 250,000 customers across the world. It has built a strong reputation, featuring at 38 in Top 100 Innovative Companies in the World by Forbes 2011-2018.

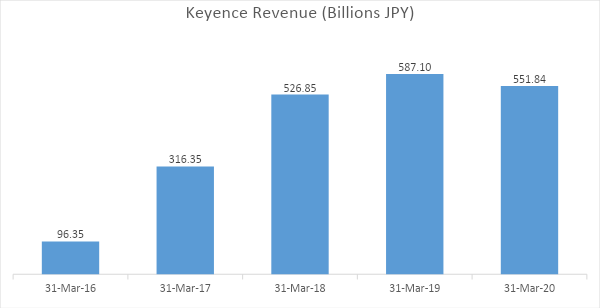

Keyence has displayed tremendous revenue growth growing its revenues by more than 6x in 5 years.

It has achieved this phenomenal growth without compromising on the margins which are fairly high at 50% operating profit margin and 36% Net Profit Margin.

| All figures in Billions JPY except EPS and Ratios | 31-Mar-20 | 31-Mar-19 | 31-Mar-18 | 31-Mar-17 | 31-Mar-16 |

| Revenue | 551.84 | 587.10 | 526.85 | 316.35 | 96.35 |

| Gross Profit | 451.44 | 483.47 | 432.67 | 255.87 | 77.48 |

| Depreciation | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Interest | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Operating Income | 277.63 | 317.87 | 292.89 | 169.75 | 49.16 |

| PAT | 198.12 | 226.15 | 210.60 | 120.68 | 32.48 |

| EPS | 816.91 | 932.45 | 868.33 | 497.55 | 267.78 |

| Gross Margin | 82% | 82% | 82% | 81% | 80% |

| Operating Margin | 50% | 54% | 56% | 54% | 51% |

| Net Profit Margin | 36% | 39% | 40% | 38% | 34% |

| Current Assets | 1,149 | 1,078 | 1,023 | 842 | 859 |

| Cash | 944 | 863 | 808 | 677 | 711 |

| Current Liabilities | 75 | 86 | 98 | 60 | 45 |

| LT Debt | 0 | 0 | 0 | 0 | 0 |

| Equity | 1,758 | 1,588 | 1,381 | 1,185 | 1,066 |

| ST Debt | 0 | 0 | 0 | 0 | 0 |

| Maturity of LT | 0 | 0 | 0 | 0 | 0 |

| Current Ratio | 15.242 | 12.594 | 10.490 | 14.015 | 19.291 |

| Debt to Equity | 0 | 0 | 0 | 0 | 0 |

| Cash to Equity | 0.07 | 0.07 | 0.06 | 0.05 | 0.06 |

Its unique business model of outsourcing manufacturing allows it to enjoy these high margins without taking on any debt or leverage. It is a zero debt company with significant current assets to take care of their liabilities.

The world demand for automation is about to accelerate exponentially as factories begin to realize the need to operate without staff both in order to cut costs as well as to comply with the new regulations. One can see this being advantageous to Keyence due to it being a market as well as cost leader in manufacturing.

OBIC Co Ltd.

OBIC is an IT technology company headquartered in Japan and offering products in customized optimal software, pc-peripherals and telecommunication equipment.

Its services include computer system integration services, system support services, office automation and package automation. Its network of offices is spread across Hiroshima, Saitama, Aichi, Shizuoka and Kyoto

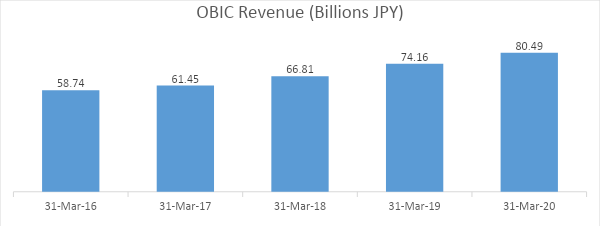

OBIC has displayed steady revenue growth and high margins for a commoditized business.

| All figures in Billions JPY except EPS and Ratios | 31-Mar-20 | 31-Mar-19 | 31-Mar-18 | 31-Mar-17 | 31-Mar-16 |

| Revenue | 80.49 | 74.16 | 66.81 | 61.45 | 58.74 |

| Gross Profit | 56.33 | 50.94 | 44.52 | 39.84 | 37.52 |

| Depreciation | 0.15 | 0.11 | 0.11 | 0.11 | 0.12 |

| Interest | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Operating Income | 44.86 | 40.00 | 33.08 | 28.05 | 28.78 |

| PAT | 35.10 | 32.22 | 26.27 | 23.36 | 23.16 |

| EPS | 381.21 | 345.31 | 289.17 | 261 | 237.86 |

| Gross Margin | 70% | 69% | 67% | 65% | 64% |

| Operating Margin | 56% | 54% | 50% | 46% | 49% |

| NPM | 44% | 43% | 39% | 38% | 39% |

| Current Assets | 141.16 | 131.13 | 119.59 | 110.07 | 93.71 |

| Cash | 129.61 | 119.97 | 109.46 | 98.12 | 82.50 |

| Current Liabilities | 18.44 | 18.98 | 16.67 | 15.57 | 14.28 |

| LT Debt | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Equity | 238.39 | 218.48 | 197.39 | 177.50 | 160.52 |

| ST Debt | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Maturity of LT | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Current Ratio | 7.65 | 6.91 | 7.17 | 7.07 | 6.56 |

| Debt to Equity | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Cash to Equity | 0.07 | 0.06 | 0.06 | 0.05 | 0.04 |

Its high margins have improved continuously. It is a zero debt company with limited liabilities and a high level of current assets. With the uptrend of Work from Home policies, demand for computers and peripherals like Monitors, headphones, mouse and keyboard is high and is bound to increase further as more companies adopt the this culture.

Telecommunication is also expected to experience a boom as the need for high speed connectivity rises across small towns and villages. This double demand increase is expected to benefit OBIC who operates in these segments giving its prospects a further boost.

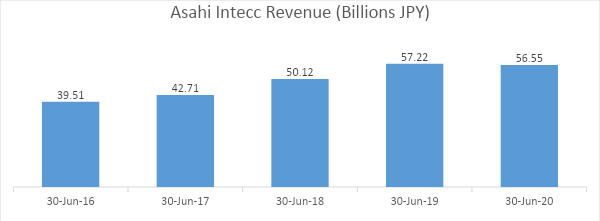

Asahi Intecc Co. Ltd.

Asahi Intecc is engaged in the manufacturing of medical tools as well as both medical and industrial use stainless steel ropes.

Its product line includes catheters, guide wires, miniature coils for endoscopic devices etc. It has 6 branches across the world including Europe as well as supply tie ups with companies across the globe.

The company has seen decent revenue growth and healthy profit margins.

It has little debt and a debt to equity ratio of 0.12. Its cash exceeds its current liabilities and company has an excellent current ratio as well.

| All figures in Billions JPY except EPS and Ratios | 30-Jun-20 | 30-Jun-19 | 30-Jun-18 | 30-Jun-17 | 30-Jun-16 |

| Revenue | 56.55 | 57.22 | 50.12 | 42.71 | 39.51 |

| Gross Profit | 38.04 | 39.70 | 34.86 | 28.43 | 25.92 |

| Depreciation | 0.94 | 0.83 | 0.64 | 0.54 | 0.51 |

| Interest | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Operating Income | 12.79 | 15.29 | 13.57 | 10.64 | 9.69 |

| PAT | 9.18 | 11.24 | 10.04 | 7.73 | 6.91 |

| EPS | 34.03 | 43.05 | 39.22 | 30.81 | 55.27 |

| Gross Margin | 67.27% | 69.39% | 69.54% | 66.56% | 65.59% |

| Operating Margin | 22.62% | 26.73% | 27.08% | 24.92% | 24.53% |

| Net Profit Margin | 16.23% | 19.64% | 20.03% | 18.09% | 17.48% |

| Current Assets | 47.79 | 45.82 | 42.06 | 39.72 | 30.35 |

| Cash | 18.55 | 18.78 | 19.16 | 19.99 | 12.94 |

| Current Liabilities | 12.79 | 12.62 | 12.39 | 12.29 | 9.38 |

| LT Debt | 5.69 | 3.28 | 3.77 | 3.52 | 6.36 |

| Equity | 71.95 | 65.43 | 53.60 | 44.66 | 32.26 |

| ST Debt | 1.44 | 1.15 | 0.87327 | 0.8848 | 0.81299 |

| Maturity of LT | 1.64 | 2.04 | 2.05 | 3.88 | 2.28 |

| Current Ratio | 3.74 | 3.63 | 3.39 | 3.23 | 3.24 |

| Debt to Equity | 0.12 | 0.10 | 0.12 | 0.19 | 0.29 |

| Cash to Equity | 0.02 | 0.02 | 0.02 | 0.02 | 0.03 |

The company dominates in cardiovascular systems. As per WHO, cardiovascular deaths are the number 1 cause of lifestyle related deaths globally taking an estimated 17.9 million lives each year. This number is expected to increase as people spend more and more of their time in the house sitting on the chair or couch. Asahi’s dominance in this segment allows it to capture decent market share. They have also announced their desire to foray into other areas like peripheral vascular, abdominal and cerebrovascular areas as well. This expansion into other areas will help improve future prospects for Asahi Intecc.

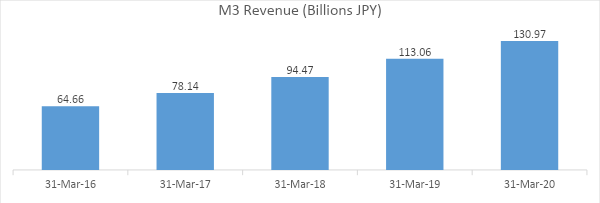

M3 Inc.

Unlike its similar namesake 3M, M3 Inc. is a provider of medical related services through the use of Internet. Its services are used by physicians, pharmaceutical companies and other healthcare professionals. M3 represents the three M’s of Medicine, Media and Metamorphosis.

Its business is categorized into Medical Platform, Evidence Solution, Career Solution, Overseas and other Emerging Business. Some of its products include AskDoctors, MDLinx and iTicker Plus. It has five million memberships and 2,70,000 physicians using its services. It operates in Japan, US, UK, India, Spain, Germany, France, China and Korea.

M3 has experienced phenomenal revenue growth doubling its revenue in 5 years while maintaining healthy margins. It has very little debt and sufficient reserves to take care of is liabilities. It also prides itself in innovative products which keep their customers engaged.

| All figures in Billions JPY except EPS and Ratios | 31-Mar-20 | 31-Mar-19 | 31-Mar-18 | 31-Mar-17 | 31-Mar-16 |

| Revenue | 130.97 | 113.06 | 94.47 | 78.14 | 64.66 |

| Gross Profit | 72.89 | 63.84 | 53.75 | 46.04 | 37.69 |

| Depreciation | 3.13 | 0.96 | 0.73 | 0.60 | 0.54 |

| Interest | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Operating Income | 34.34 | 30.80 | 27.49 | 25.05 | 20.02 |

| PAT | 24.15 | 21.35 | 19.23 | 16.94 | 13.49 |

| EPS | 32.57 | 29.43 | 27.6 | 24.8 | 19.12 |

| Gross Margin | 56% | 56% | 57% | 59% | 58% |

| Operating Margin | 26% | 27% | 29% | 32% | 31% |

| Net Profit Margin | 18% | 19% | 20% | 22% | 21% |

| Current Assets | 121.55 | 63.99 | 53.60 | 41.81 | 38.87 |

| Cash | 70.98 | 33.15 | 26.18 | 21.22 | 22.93 |

| Current Liabilities | 38.14 | 28.00 | 24.56 | 20.55 | 14.99 |

| LT Debt | 4.67 | 0.32 | 0.42 | 0.04 | 0.05 |

| Equity | 166.11 | 98.73 | 82.48 | 67.06 | 54.89 |

| ST Debt | 0.00 | 0.00 | 0.00 | 0.00 | 0.06 |

| Maturity of LT | 2.56 | 0.36 | 0.06 | 0.10 | 0.91 |

| Current Ratio | 3.186 | 2.285 | 2.183 | 2.035 | 2.592 |

| Debt to Equity | 0.044 | 0.007 | 0.006 | 0.002 | 0.019 |

| Cash to Equity | 0.012 | 0.006 | 0.005 | 0.004 | 0.004 |

Digital Health Consultancy has made significant inroads in 2020 with patients requiring doctor’s advice but unable to visit physically having adopted digital consultancy mechanisms. The ease of use, elimination of travel to doctor’s office, quick and fast consultancy in the comfort of your home and reasonable rates will ensure increased adoption of digital health consultancy thus benefiting M3 who has dominance in this segment. The digital health market is expected to grow from 106 billion USD in 2019 to 640 billion USD in 2026 at a healthy CAGR of 28.5% and M3 is expected to grab a slice of that.